Retirement is a time to enjoy the fruits of your labor, but taxes can take a significant bite out of your savings if you’re not prepared. Learning how to plan for taxes in retirement is essential to ensure your financial security and peace of mind. This guide will walk you through actionable strategies to minimize your tax burden, optimize your income, and make your retirement years truly golden. Whether you’re nearing retirement or already there, these tips will help you navigate the complex world of retirement taxes with confidence.

Why You Need to Plan for Taxes in Retirement

Taxes don’t disappear when you retire—they just change. Social Security benefits, pension withdrawals, and investment income can all be taxable, and poor planning can lead to unexpected tax bills. According to the IRS, up to 85% of your Social Security benefits may be taxable depending on your income. By proactively planning for taxes in retirement, you can avoid surprises and keep more of your hard-earned money.

The Cost of Ignoring Retirement Tax Planning

Failing to plan can result in higher tax liabilities, reduced savings, or even penalties. For example, Jane, a retiree in Florida, didn’t account for taxes on her 401(k) withdrawals. She was shocked to owe $12,000 in taxes after withdrawing a lump sum for a home renovation. Strategic tax planning could have spread out her withdrawals to stay in a lower tax bracket.

Key Strategies to Plan for Taxes in Retirement

Here are proven strategies to help you minimize taxes and maximize your retirement income.

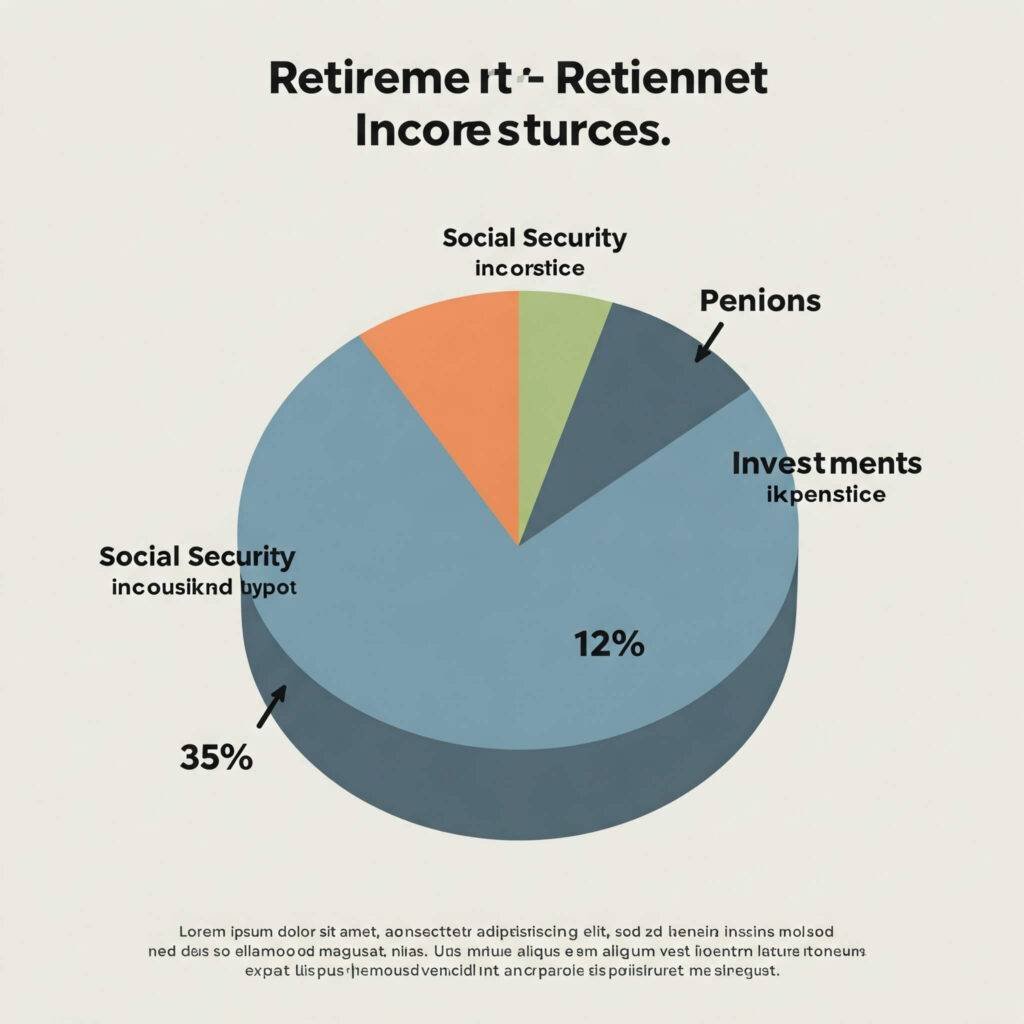

1. Understand Your Retirement Income Sources

To plan for taxes in retirement, you need to know which income sources are taxable. Common sources include:

- Social Security Benefits: Taxable if your combined income exceeds $25,000 (single) or $32,000 (married filing jointly).

- Pension Income: Usually fully taxable unless contributions were made with after-tax dollars.

- 401(k) or Traditional IRA Withdrawals: Taxed as ordinary income.

- Investment Income: Capital gains and dividends may be taxed, depending on your accounts.

Actionable Tip: Use a retirement income calculator to estimate your taxable income and plan withdrawals.

2. Leverage Tax-Advantaged Accounts

Tax-advantaged accounts like Roth IRAs and Health Savings Accounts (HSAs) can reduce your tax burden in retirement.

- Roth IRA: Withdrawals are tax-free after age 59½, provided the account has been open for five years.

- HSA: Contributions are tax-deductible, and withdrawals for qualified medical expenses are tax-free.

- Traditional IRA or 401(k): Consider converting to a Roth IRA gradually to manage taxes over time.

Real-World Example: Tom, a 62-year-old retiree, converted $20,000 annually from his traditional IRA to a Roth IRA over five years. By spreading out the conversions, he stayed in a lower tax bracket and now enjoys tax-free withdrawals.

Outbound Link: Learn more about Roth conversions at Fidelity.

3. Manage Withdrawals to Stay in Lower Tax Brackets

Strategic withdrawal planning can keep you in a lower tax bracket. For 2025, the federal income tax brackets for married couples filing jointly are:

- 10% for income up to $23,200

- 12% for income up to $94,300

- 22% for income up to $201,050

Actionable Tip: Withdraw just enough from taxable accounts to stay within the 12% bracket, then supplement with tax-free income like Roth IRA withdrawals.

4. Optimize Social Security Benefits

Timing your Social Security benefits can significantly impact your taxes. Delaying benefits until age 70 increases your monthly payout and may reduce your taxable income in early retirement years.

Actionable Tip: If you have other income sources, delay Social Security to minimize the taxable portion of your benefits.

Outbound Link: Explore Social Security strategies at AARP.

5. Plan for Required Minimum Distributions (RMDs)

Starting at age 73, you must take RMDs from traditional IRAs and 401(k)s. These withdrawals are taxable and can push you into a higher tax bracket.

Actionable Tip: Consider Qualified Charitable Distributions (QCDs) to satisfy RMDs tax-free by donating directly to a charity.

Common Mistakes to Avoid When Planning for Taxes in Retirement

- Withdrawing Large Lump Sums: This can spike your taxable income and push you into a higher tax bracket.

- Ignoring State Taxes: Some states tax Social Security or retirement income. Check your state’s rules via the Tax Foundation.

- Not Consulting a Professional: A tax advisor or financial planner can tailor strategies to your unique situation.

Take Control of Your Retirement Tax Plan Today

Planning for taxes in retirement doesn’t have to be overwhelming. By understanding your income sources, leveraging tax-advantaged accounts, managing withdrawals, and avoiding common pitfalls, you can keep more of your savings and enjoy a financially secure retirement. Start by reviewing your retirement accounts and consulting a financial advisor to create a personalized tax strategy.

Call to Action: Ready to take charge of your retirement taxes? Use a free tax calculator to estimate your tax liability and start planning today!

Outbound link: